Viking

-

Posts

4,644 -

Joined

-

Last visited

-

Days Won

35

(1).thumb.png.afef2977f5053cb2dd62f46c5f452643.png)

Viking's Achievements

")

-

@Mystery Guest , I think you might be on to something. Fairfax compounded book value at 18.4% for 38 straight years. That is a phenomenal track record. To call the company ‘no-moat’ is, of course, idiotic. Obviously, there is a moat hiding in there somewhere.

-

I do not follow Fairfax India as closely as i follow Fairfax. The big near term issue that i see is IIFL Finance - but this has been out there for months now so it should not have come as a surprise when Fairfax India reported results. What did surprise me is the explanation of the current issues the founder of IIFL, Nirmal Jain, gave at the Fairfax India AGM (see quote below). The answer he gave might come across as funny to an audience in India. I don’t think it’s the right kind of humour to use when explaining a serious problem to an audience in North America. Hopefully Fairfax uses this as an example internally of probably what not to do in the future. —————- “So RBI does (our) audit, and they've been doing it for the last 16 years of our company's existence. And this year, they found a few lapses. And based on that, we're a bit surprised because the order came, which was a complete embargo on our gold loan business. And of course, there were lapses. So I can't say that it's something which is -- we are doing everything which was in full compliance of their master circular. “But many of these things that we are doing were also industry practice. So maybe I can give analogy. I mean I don't know many of you would have traveled to India there, the traffic rules are hardly followed. The people obviously. Now -- but if you are in Canada, U.S. everywhere, then you see that even if the other side is empty and there's a 3-mile traffic jam, people still won't break the lane because somewhere -- some point in time, regulators enforce the regulations very strictly. “So what happens that in traffic police officer catch hold of somebody and sort of make him an example. And if we have a view, then I don't think that we can really crib about it, but I'll just talk about it that what happened and how we are going to overcome.”

-

@gamma78 and @valueinvesting101 great comments. Thanks for chiming in. I do find it interesting how aggressive Fairfax has been since 2018 in buying back Fairfax’s stock. Yes, Fairfax got the stock at a crazy low price. But this also has the effect of shrinking the size of the company. I like this - as we have learned with Berkshire, ever-increasing size eventually becomes a constraint on returns. Keeping Fairfax small (relatively) should help Fairfax deliver above average returns moving forward. Great points on India. Is the set-up today in India like the US back in the 1950’s? Buy a basket of ‘quality at a fair price’ and hang on for decades? Interesting idea. I have been a little bit surprised how quiet Fairfax has been in India the past couple of years. Their playbook there has been monetizing assets, increasing their ownership of BIAL and building cash. Like a spring getting loaded?

-

some quick thoughts: Wade’s summary was short, concise and well done. Investment portfolio is $65b; $46 fixed income and $19b equity Grivalia Hospitality - George K estimates One and Only development is worth entirety of GH carrying value. Kennedy Wilson debt platform is at $4.8b? and yield is 8.25% As fixed income matures, Fairfax has been leaving at short end, which is shortening avg duration a little. Allied World - reinsurance increased double digit Eurobank - share of profit of associates was $79 million; this included $45 million in one offs (adj due to sale of sub etc); underlying was $124 million, which was $30 million more than prior year. GIG ownership was increased in April from 90 to 97.1 at a cost of $127 million (mandatory tender offer) FFH-TRS: think its a great investment (shares still offer good value) Insurance: continue to see opportunities. Price increases exceed loss cost trends. Insurance subs have $3 billion in dividend capacity; paid $451 million to hold co in Q1. Expense ratio ticked higher in Q1: inclusion of GIG (has higher exp ratio), bus mix, investments in technology

-

The $1 billion bond offering closed late in March. My assumption is Fairfax will start paying interest immediately. As a result, my assumptions is they also have use of the $1 billion. If they do not have an immediate use for the $1 billion my assumption is they could buy very short term treasuries with it. if they did this we would see a small increase in interest income. $1 billion earning 5% = $50 million = $1 million per week. Now if I am way off base (perhaps my 5% is way too high?), please let me know (it wouldn’t be the first time).

-

@Spooky I think you are missing the point of my post. I don’t say this to be a jerk /confrontational. “Which investments in Fairfax's portfolio today are wonderful companies (i.e. high return on assets and growing) that can just keep compounding at high rates of return for the next 20-30 years?” Here is a re-post of what i said earlier: Investors waiting for Fairfax to buy ‘Coke’ or ‘American Express’ in 2024 will likely be sorely disappointed. For two reasons: 1.) Buffett’s brilliance wasn’t buying Coke or American Express. It was exploiting the set of circumstances that existed at the time, which served up Coke in 1988 and AMEX in 1990. 2.) Like Berkshire when it made its many brilliant moves, most investors probably won’t see it when Fairfax actually does it. Moving forward, i expect Fairfax to use ALL the capital allocation levers at their disposal. You list one above - and i do expect them to do more of that. But i also expect Fairfax to do lots of other things. Some will likely be non-traditional. What they do will largely be driven by volatility and what opportunities get served up. But in terms of ‘buying quality at a reasonable price’, on the equity side, I think their investment in BIAL would be a good recent example. Buying Allied World in 2017 for $4.9 billion would be a good recent insurance example. Fairfax’s equity book as a whole has improved significantly in quality over the past 5 years. The best example is Eurobank. Is it a quality bank today? Yes. Is it cheap? Yes. Is it poised to deliver excellent returns over the next 5 years? Yes, i think so. Is Eurobank like Coca Cola or AMEX back in the late 1980’s? No, of course not. You appear to give the two examples i provided (effectively buying back 23% of shares outstanding at 30% of current intrinsic value and a saving/earning billions from active management of their fixed income portfolio) as not really counting. I humbly disagree. Of course, that’s what makes for a great debate. When I say i think Fairfax resembles a much younger Berkshire Hathaway, it might help if i spell out what that might mean from a return perspective. If my thesis is correct, below is what i think is possible. (Of course, my thesis could be completely wrong - and this would mean my return expectations below would also be completely wrong.) Since inception Berkshire Hathaway has materially outperformed the S&P500 (dividends included). I think Berkshire’s outperformance might be 2x. I think Fairfax is poised to materially outperform the market indices over the next 5 years (I would take an average of the S&P500 and the TSX60). I think Fairfax’s outperformance could come in at 2x better. Similar to Berkshire Hathaway’s long term average level of outperformance. How will Fairfax do it? I think the set-up today for Fairfax looks a lot like a much younger Berkshire Hathaway. In my post above, i highlighted 14 factors that i thought were similar. For me this is more qualitative/philosophical type thinking than quantitative/precise type thinking. And this makes it very hard to discuss/debate - because everyone comes at it in a very different way.

-

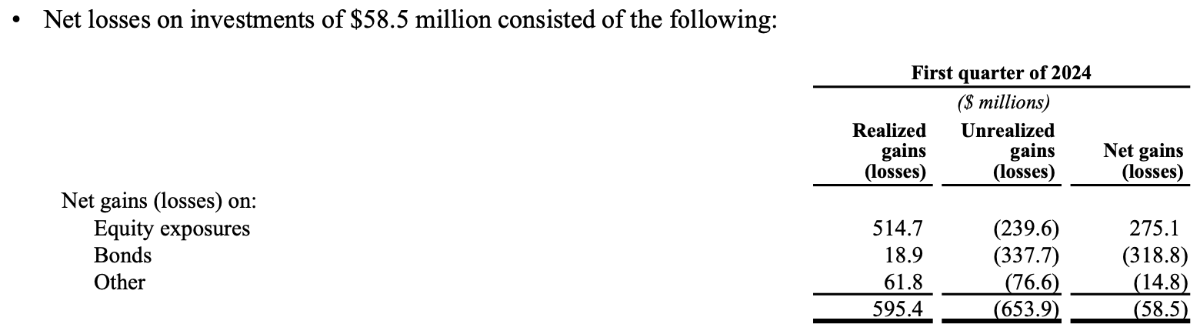

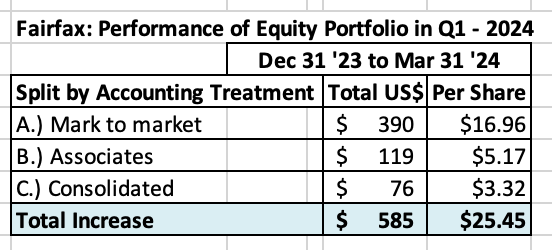

Q1 Earnings: Answers to questions Overall, it was a boring, solid quarter. 1.) How are they allocating new capital? What did Fairfax do with $1 billion notes offering that was completed the end of March? A: Stay tuned. Cash increased to $2.5 billion. It is earning +5% so perhaps Fairfax feels no urgency to deploy it quickly. 2.) Impact of change in interest rates on reported results? A: this was about a $125 million headwind. This was higher than I expected; although I do expect the puts and takes to roughly balance out over time. "The benefit of the effect of increases in discount rates on prior year net losses on claims of $192.3 million partially offset net losses recorded on the company’s bond portfolio of $318.8 million." 3.) What is interest and dividend income? Q4, 2023 = $536.4 million Q1, 2024 = $589.8 million = a run rate of $2.36 billion for 2024 (up from $1.9b in 2023). A: Increased $53 million from last quarter. Much more than I was expecting. Is Fairfax’s investment in Kennedy Wilson’s debt platform continuing to grow? A: Yes. It increased by $160 million in Q1. 4.) Insurance What is growth in net premiums written? GIG + organic? A: Solid increase of 11.2% (5.3% was GIG) What is CR? Is it below 94%? A: Solid 93.6% (was 94.0% in Q1, 2023) What is level of reserve releases? Trend? A: TBD Brit update: ex Ki, CR was 90.2% in Q1. Importantly, company is growing top line again, as net premiums written increased 6.5% in Q1. Continuing solid performance we saw in 2023. 5.) What is share of profit of associates? A: Total of $127.7 was lower than expected. $28.6 million loss from Helios. Seasonality. Not concerned. "Consolidated share of profit of associates of $127.7 million principally reflected share of profit of $79.3 million from Eurobank, $36.0 million from EXCO Resources and $34.8 million from Poseidon, partially offset by share of loss of $28.6 million from Helios Fairfax Partners." 6.) Equities: What are investment gains from equities? A: Equities booked a $275 million gain. About what I expected (a little lower based on my tracking model but it does not capture everything Fairfax owns). For Associate holdings, what is the excess of market value to carrying value? Q1, 2024 = $1,185.6 million = $52/share 7.) Is there any adverse development for runoff? More broadly, what are the results for runoff/life bucket? A: Results were roughly as expected. 8.) What is book value per share? This increased a smaller amount than I expected; normal range. The dividend payment in January will dent this by $15/share. Q1 = $945.44 (2023YE = $939.65) 9.) Other notes: Shares Outstanding During the first quarter of 2024 the company purchased 240,734 of its subordinate voting shares for cancellation at an aggregate cost of $260.3 million ($1,081/share). Fairfax is now buying back shares at a premium to book value. They continue to see this as an attractive price to pay. At March 31, 2024 there were 22,831,173 common shares effectively outstanding. Interest expense Was $151.5 million in Q1; about $20 million more than I expected. And it does not include a full quarter of the $1 billion in new borrowings that closed in late March (while this is being held, the interest being earned will show up in interest income). Comprehensive income Unrealized foreign currency translation losses were $228.4 million in Q1. Yes, the US$ was very strong.

-

What were the key drivers of Berkshire Hathaway’s success when the company was in its prime? I have ranked the key drivers by importance. Did i get the list right? What is missing? Did i get the order right? If not, what is the new order? 1.) Buffett the man is a genius. As an investor. He has also been a very good manager. 2.) Control - Buffett has voting control. Gave Buffett free rein to run the company as he saw fit Without this, Berkshire Hathaway never would have evolved as it did 3.) Capital allocation skills of management. Primarily Buffett, but also includes Charlie Munger, Ajit Jain, Greg Abel etc. Value investing framework: shifted over the years (as Berkshire Hathaway grew in size) from deep value to quality at a reasonable price 4.) Insurance Float Provides a low cost, stable and growing source of funds/capital that Buffett used to make many outstanding investments. When combined with 3.) magnified returns. Float loses its value when interest rates are very low, like they were from 2010-2020. Float increases greatly in value when interest rates are high like they are today. 5.) Long term focus Fits hand and glove with the ‘buy and hold’ value investing framework. Investments: able to take advantage of market volatility. Also fits hand in glove with the P/C insurance cycle - which can run in 15 year cycles (hard to soft and back to hard). 6.) Invest a significant portion of the investment portfolio in equities. Embrace volatility Earn a much higher return, compared to a bond only portfolio. 7.) Culture Insurance and investments - operations decentralized Capital allocation - managed by Buffett / small corporate office 8.) Businesses generated enormous cash flow. Both insurance and investments: was reinvested well, creating new income streams. Virtuous circle. 9.) The company was small. capital allocation decisions made had a relatively quick and material impact on the performance of the company 10.) Power of compounding Attributes 1 to 9 - all happening at the same time - is a very powerful elixir, especially if it can be maintained for decades. time is the friend of the wonderful business 11.) Favourable external environment There was lots of volatility in financial markets. This provided continuous supply of opportunities to deploy large amounts of capital at very attractive rates of return.

-

@Xerxes you have a wicked sense of humour. I laughed out loud when i read your post and saw the picture.

-

Comparing Berkshire Hathaway with Fairfax Financial - some thoughts. When Buffett first bought AMEX and Coca-Cola were they viewed at the time like they were brilliant investments? No, of course they weren’t. It often takes a decade or longer - after the purchase - to evaluate/appreciate a brilliant capital allocation decision. Example 1 From 2018-2023, Fairfax invested $2 billion and now owns 15.5% of a high quality company. The average price paid that was about 1/3 of its current intrinsic value (conservatively valued). They bought high quality at an exceptionally low price. And they backed up the truck - $2 billion is a lot of money (at the time, common shareholders equity was around $13 billion). But the story gets even better. In late 2020/2021, Fairfax got exposure to another 7.5% of the very same high quality company. This time they paid about 28% of current intrinsic value. In total, they ‘purchased’ about 23% of this company, paying on average about 30% of current intrinsic value. This investment is poised to compound at mid to high teens in the coming years. Hello people… have you been paying attention? (Yes, the company they bought is called Fairfax.) Example 2 In Q4 2021, Fairfax sold most of their corporate bonds and dropped the average duration of their fixed income portfolio to 1.2 years. In Q4 2023 they extended the average duration of their fixed income portfolio to +3 years. What they did with their fixed income portfolio saved the company $3 billion? (or more?) in unrealized bond losses. Because duration was so short, the earn through from spiking interest rates was immediate in 2022 and 2023. Today they are earning $2 billion in interest income and it is now largely locked in for the next 4 years. They protected their balance, pivoted and are now earnings record interest and dividend income - the highest quality income stream a P/C insurer can have. Fairfax’s financial profile (and future) has been permanently changed (improved) as a result of these actions. Ask AM Best if you don’t believe me. The parallels with a much younger Berkshire Hathaway “History does not repeat itself, but it rhymes.” Mark Twain Investors waiting for Fairfax to buy ‘Coke’ or ‘American Express’ in 2024 will likely be sorely disappointed. For two reasons: 1.) Buffett’s brilliance wasn’t buying Coke or American Express. It was exploiting the set of circumstances that existed at the time, which served up Coke in 1988 and AMEX in 1990. 2.) Like Berkshire when it made its many brilliant moves, most investors probably won’t see it when Fairfax actually does it. How do I know this? Because Fairfax has been making exceptional capital allocation decisions for years now. For a couple of these they got out their elephant gun. And they still get no (little) credit. And that is because the company continues to be misunderstood. The moves Fairfax has been making continue to be grossly under appreciated. Just like when Buffett made his great investments, investors need more time to fully appreciate the brilliance of what Fairfax has executed in recent years. If lots of people on this board don’t see it… do you think the rest of the investor community does? That’s why the stock trades at 1.1x book value - crazy cheap. The key lesson for investors The world is different today - the set of circumstances is ever changing. Importantly, with normalized - higher - interest rates, volatility in financial markets is back. We had bear markets in stocks in 2020 and again in 2022. We had a historic bear market in bonds in 2022. And just look at what Fairfax has been doing. Most investors still can’t see what is right in front of their face. Because they are looking for the wrong thing. Active management can have a huge impact on financial results. Now most P/C insurance companies don’t actively manage their investment portfolio. Fairfax does. Fairfax today: 1.) They are run by a genius - yes, anyone who can compound book value at 18.4% for 38 years is a genius. What is Prem’s greatest strength? Perhaps his ability to attract and retain talent, beginning with the creation of Hamblin Walsa 38 years ago and continuing with the guys running insurance like Andy Barnard. 2.) They are family controlled - importantly, this allows for long term decision making. Along the same line, this also allows them to take full advantage of volatility, even if it takes some time to work out. 3.) They have Hambin Watsa - handles all capital allocation decisions. 4.) Capital allocation - They use a value investing framework. This appears to be evolving over time. Today, they appear to be placing more of a premium on management. And financial strength/profitability. ‘Quality at a fair price’ versus classic Graham ‘deep value’ type investing. 5.) They are highly levered to float. Its cost is better than free (they are actually getting paid to hold it) and it is growing in size. 6.) Culture - insurance and investments are run on a decentralized model. 7.) They invest a large part of their investment portfolio in equities. Most traditional P/C insurance companies stick to fixed income investments. 8.) They are still a small company - this gives them a very large opportunity set. 9.) They have their elephant gun out. 10.) They are able to move with speed. 11.) They have been generating an enormous amount of cash the past couple of years and this is set to continue in the coming years (net earnings of around $4 billion per year?). 12.) They are on a hot streak - when it comes to capital allocation. 13.) And volatility - more normal financial markets - is back. So lots of opportunities will be coming in the future. 14.) Compounding - as always - sits ready to work its magic. This set-up looks an awful lot like a much younger Berkshire Hathaway. But what Fairfax does/how they execute will likely not look anything like what Berkshire Hathaway did back in the 1980’s. And that is because history does not repeat exactly. But it sometimes rhymes. And I think this might be one of those times. Today, Berkshire Hathaway is like an aging elephant. And Fairfax is like a lion in its prime. And the drought (zero interest rates) has ended - and the savannah is once again teeming with game.

-

For Berkshire (and Fairfax) i think the cash drag was more a problem when short term interest rates were effectively zero. Now that short term rates are much higher (3 month treasury is 5.4%) holding cash is no longer a drag on returns.

-

Fairfax of 10 years ago looks little like the Fairfax of today. So many ‘Fairfax pundits’ from 10 years ago do not recognize this change. There have been two game changers that have played out/accelerated over the past 4 years: 1.) capital allocation: the senior team at Fairfax has hit the ball out of the park the past 4 years. It is surfaced billions in shareholder value. 2.) the size of the increase in operating cash flow - and the fact it is largely locked and loaded for the next 4 years. As a result, Fairfax is now entering uncharted territory as a company (for it). We are all still learning what baseline earnings are. The financial positioning/quality of the company has improved markedly. The bond ratings agencies (AM Best - insurance specialists) are ahead of the equity analysts in this regard - which is surprising (to me at least). The people who are likely at the biggest disadvantage when it comes to Fairfax today are those who believed in the company and then bailed in 2018 to 2020 (stop the pain). And the detractors / haters. These investors/groups have the most to unlearn. ————— Fairfax’s business and its future prospects have undergone a paradigm shift the past 4 years. One that many smart people don’t fully grasp today. “The disadvantage of a mind-set is that it can color and control our perception to the extent that an experienced specialist may be among the last to see what is really happening when events take a new and un-expected turn. When faced with a major paradigm shift, analysts who know the most about a subject have the most to unlearn. This seems to have happened before the reunification of Germany, for example. Some German specialists had to be prodded by their more generalist supervi- sors to accept the significance of the dramatic changes in progress toward reunification of East and West Germany.” Page 5, Psychology of Intelligence Analysis by Richards J. Heuer, Jr. PDF copy of the book can be downloaded for free: https://www.ialeia.org/docs/Psychology_of_Intelligence_Analysis.pdf

-

@dartmonkey , i think there are 2 keys when comparing Fairfax and Berkshire today: 1.) leverage: Fairfax is much more levered to float. All things being equal, that should contribute to outperformance. 2.) size: Fairfax is much smaller. The opportunities available to it are much larger. AND the impact of good decisions will have a much quicker and larger impact on reported results. For proof, all you have to do is look at capital allocation at Fairfax and Berkshire Hathaway over the last 4 years. There is no comparison. That is not being critical of Berkshire Hathaway - it is an aging elephant.

-

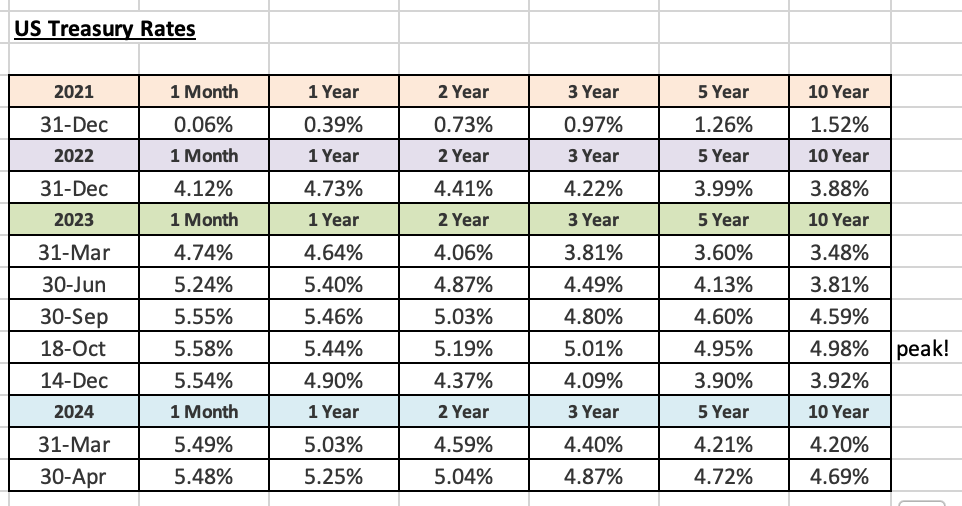

Q1 Earnings Preview. Below are a few of the things i will be watching for when Fairfax reports after markets close on Thursday. Anything missing from my list? 1.) How is Fairfax allocating new capital? What did Fairfax do with $1 billion notes offering that was completed the end of March? Fairfax also received a $175 million dividend payment from Brit later in March. Fairfax has some pretty big cash outlays in Q1: Dividend ($15/share) = $375 million Stock buybacks = $125 million? 125,000 shares @ $1,000/share? Do we see Fairfax buy back another chunk from one of their minority partners in Brit, Allied or Odyssey? 2.) Impact of change in interest rates on reported results? US Treasury rates 2 years + out on the curve moved about 30 basis points higher in the quarter. This will be a headwind to fixed income (resulting in unrealized investment losses) but will be a tailwind to IFRS 17 reporting (resulting in a benefit). How will it all shake out? Not sure - but not concerned. I think Fairfax’s average duration is about as follows: Fixed income = 3 years Insurance liabilities = 4 years More importantly, the significant increase in bond yields since Dec 31, 2023 is giving the fixed income team at Fairfax another juicy opportunity to extend duration at pretty attractive rates. Bond yields 3 years and further out have increased about 70 basis points over the past 4 months. Bond yields are only 15 to 30 basis points from the highs they reached in mid-October 2023. 3.) What is interest and dividend income? Interest and dividend income came in at $536.4 million in Q4. Is it still increasing quarter over quarter? The Q1 number x 4 will provide the best estimate for full year interest and dividend income. Is Fairfax’s investment in Kennedy Wilson’s debt platform continuing to grow? 4.) Insurance What is growth in net premiums written? GIG + organic… What is CR? Is it below 94%? What is level of reserve releases? Trend? Commentary on hard market? 5.) What is share of profit of associates? Eurobank? Chug, chug, chug? Poseidon? Do we see green shoots yet? 6.) Equities What are investment gains from equities? The equities I track suggests mark to market gains of $390 million in Q1. For Associate holdings, what is the excess of market value to carrying value? This is value that is being created by Fairfax that is not being captured in book value. 7.) What is book value per share? The dividend payment in January will dent this by $15/share.

-

@SafetyinNumbers I did not understand Fairfax's approach to using their own equity. You taught me this. Fairfax really tries to take advantage of Mr. Market's mood swings - when the shares are valued high they issue and when the shares are valued low they buy back. Especially pre-2000. This is also something they do with their equity and insurance holdings. I think it stems from having a basic value investing framework in how they do everything. Something to keep in mind moving forward.