Thrifty3000

-

Posts

550 -

Joined

-

Last visited

-

Days Won

4

3 Followers

Recent Profile Visitors

2,327 profile views

Thrifty3000's Achievements

")

-

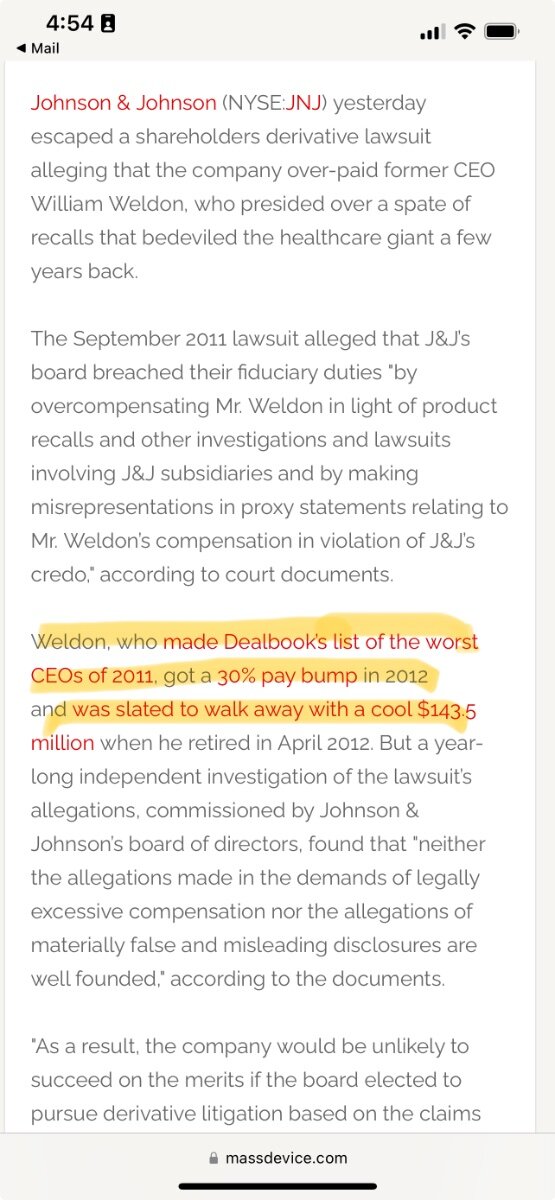

I did some digging on Weldon. Looks like he was at the center of plenty of controversy when he was at JNJ.

-

PS. I bought a few more shares today to bring my position to a nice round number. First, to make it easier/possible to do the math in my head. Haha. Second, because watching this annual meeting further cemented we're sitting on one of the most obvious lollapaloozas we'll see in our lifetimes: EXPERIENCE + INTEGRITY + CULTURE + NETWORK + SCALE + DECENTRALIZATION + GLOBAL PRESENCE + STRONG CASH FLOW + RISK PROFILE + AGILE OPPORTUNISM + CONTROLLING SHAREHOLDER + BENCH STRENGTH + FV DISCOUNT... = LOLLAPALOOZA!

-

Also, I don't think anyone should expect FFH to repurchase/retire an equivalent amount of shares upon termination of the TRS. It appears to me FFH is already using the cash payouts from the quarterly TRS gains to repurchase shares. That makes sense since they're repurchasing undervalued shares with cash proceeds from their undervalued TRS asset.

-

Regarding the TRS it sounded to me like Prem said: - all the major Canadian banks are the counterparties - the counterparties have hedging mechanisms to neutralize risk on their end - the banks can't call the TRS's before the contracted date - FFH has extended the contracts to at least 2025 (I'm not sure I heard that correctly, he may have even said 2026) - FFH can continue extending the contracts. My assumption is once FFH feels the TRS is no longer a bargain it will simply opt to not renew the contract (the exit price will factor in the underlying FFH share price as well as the carrying cost of the TRS).

-

LFG!

-

FWIW - I don't think anyone has already posted this here, and I hadn't seen it before I spent time digging on MW's site today - but on the day of the last FFH conference call Muddy Waters published a list on their website of specific questions and accounting discrepancies for Fairfax (this was separate from the original report). https://www.muddywatersresearch.com/wp-content/uploads/2024/02/Fairfax_MWQuestionsForQ423Call.pdf One example: "There is a $101.7 million discrepancy between what the acquirer reports paying for RiverStone, pro rata for Fairfax’s ownership, and the total consideration Fairfax reports receiving. The pro rata discrepancy grows to $335.4 million when looking at the cash consideration that CVC reported paying." I'm not qualified/motivated to assess the legitimacy of several of the claims. But, if anything raises an actual red flag, it might be worth asking Prem/Jen for clarification at the meeting.

-

From Jamie Dimon's annual letter... "we are prepared for a very broad range of interest rates, from 2% to 8% or even more" Notice he didn't say from 0% to 8% or even more. I believe recency bias accounts for much of Fairfax's discount to intrinsic value. Lot's of people heavily weight a return to zirp scenario in their longer term Fairfax model. Dimon lays out why he thinks 0% is off the table and why a higher rate environment is the more likely scenario. If Dimon is on the right track about rates then it seems baseline EPS estimates for FFH will be shifting closer to $200 as more investors/analysts' take zirp off the table and increase their expected portfolio yield by a couple hundred basis points.

-

I want the shares to triple overnight so I can exit and fly private the rest of my life.

-

Amazing analysis as always. Many thanks! Another datapoint investors should probably keep in mind is the fully diluted EPS. Looks like the fully diluted version of your estimates would land around: $146 per share for 2024 $149 per share for 2025 Fairfax’s share-based plans have a longer vesting period than most companies. So it’s less of a near-term concern, but something to be aware of.

-

Or, was Prem saying that he wouldn't be initiating tech investments, while the rest of the team is free to pursue tech opportunities as they see fit? That's how I interpreted it since they still have other tech investments in the portfolio.

-

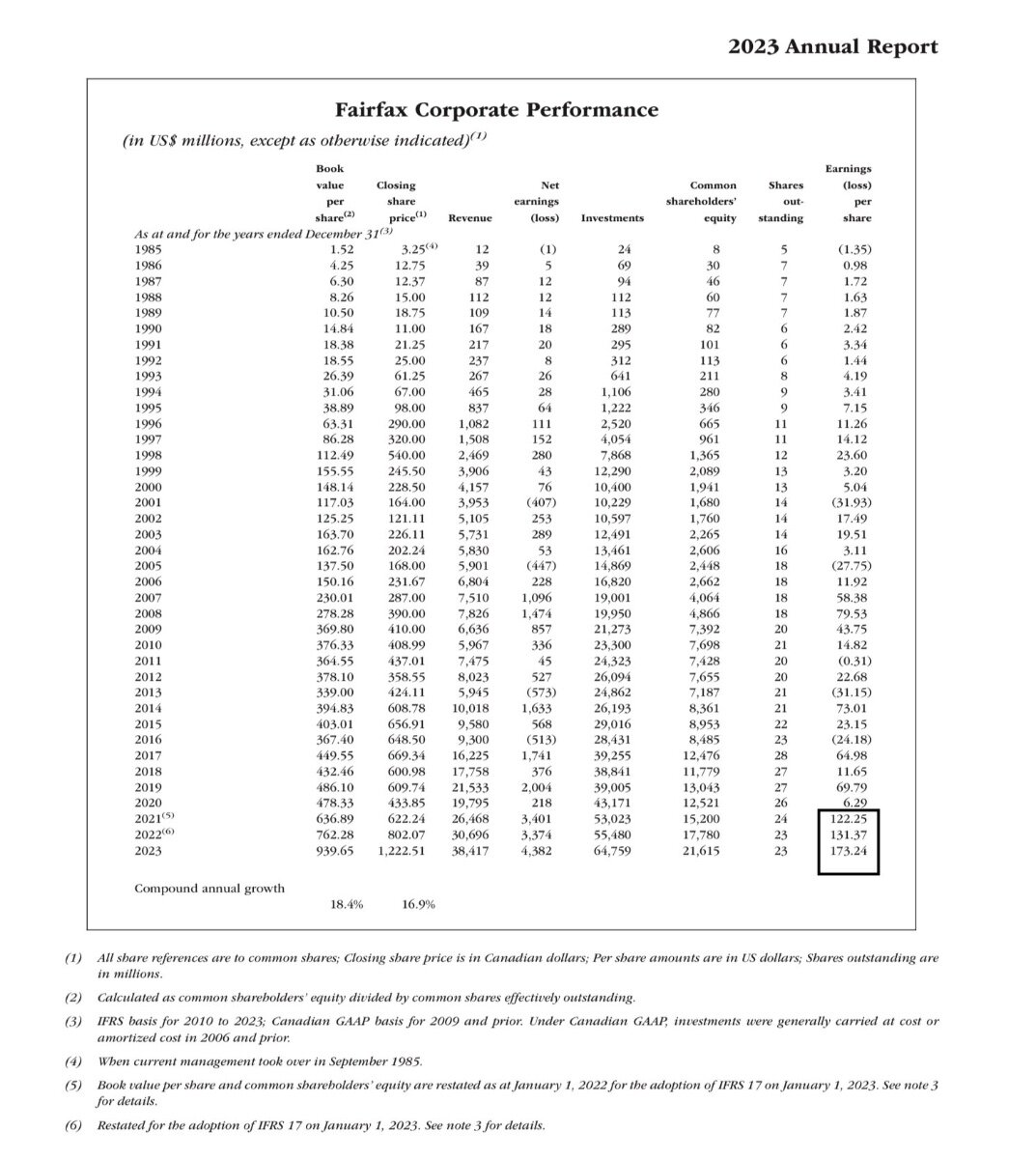

Step 1) Read this: "We had by far the best year in our history. A record underwriting profit of $1.5bn and net earnings of $4.4bn. BVPS increased 25% to US$940. In the last 3 years, our BVPS has doubled. Our operating income of $3.9bn may continue at these levels for the next 4 years.” - Prem Step 2) Study the last column, paying particular attention to the bottom right corner of this page in the annual report: Step 3) Combine knowledge gleaned from steps 1 & 2 and imagine how the chart will look four years from now. Step 4) Enjoy watching the share price climb to $2,000+ USD.

-

Elephant bumping

-

When FFH reports mind-blowing results and the stock price drops...

-

The headline was negative. The bots are doing their thing.

-

In what universe are you given ONE make-or break-question on a company’s conference call - where everyone knows your intent is to take down said company - and your ONE question is WHY DON’T YOU DISCLOSE MORE INFORMATION?? Oh brother, that was really pathetic. FFH is worth $1500 to $1800 USD per share. Kudos to Prem & Co. for a job very well done!